Insights

Explore expert geospatial insight and thought leadership

Filters (0)

- Page 1

- Insight

- Insight

- Insight

- Insight

- Insight

- Insight

- Insight

- Insight

- Insight

Climate-related flooding events threaten to cut off more towns and commuter routes across England

Ordnance Survey has identified road and rail pinch points most vulnerable to river and sea flooding.

How OS data can support the water industry to meet future demand

Discover how water companies can deliver network infrastructure to support new developments, while continuing to operate efficiently and maintain regulatory compliance.

Why location data is critical to smarter data centre planning

How trusted and accurate location data is critical to building more sustainable data centres

How location data can help identify hard to heat homes in Britain

A heat index of more than 23 million homes across Great Britain has been created using Ordnance Survey data, highlighting areas where homes are most at risk of heat loss.

Meeting the Bank of England climate standards with OS location data

How insurance and retail banking organisations can use location data to manage climate-related risks, in line with Bank of England expectations and compliance due June 2026.

Predictions for 2026 - how OS is shaping the future of geospatial technologies

Manish discusses how adopting AI is a cultural shift - and calls for renewed investment in geodesy and cartography.

Predictions for 2026 - how location data will power the next wave of infrastructure transformation

Chris shares his insight into how location data will power the next wave of infrastructure transformation in 2026.

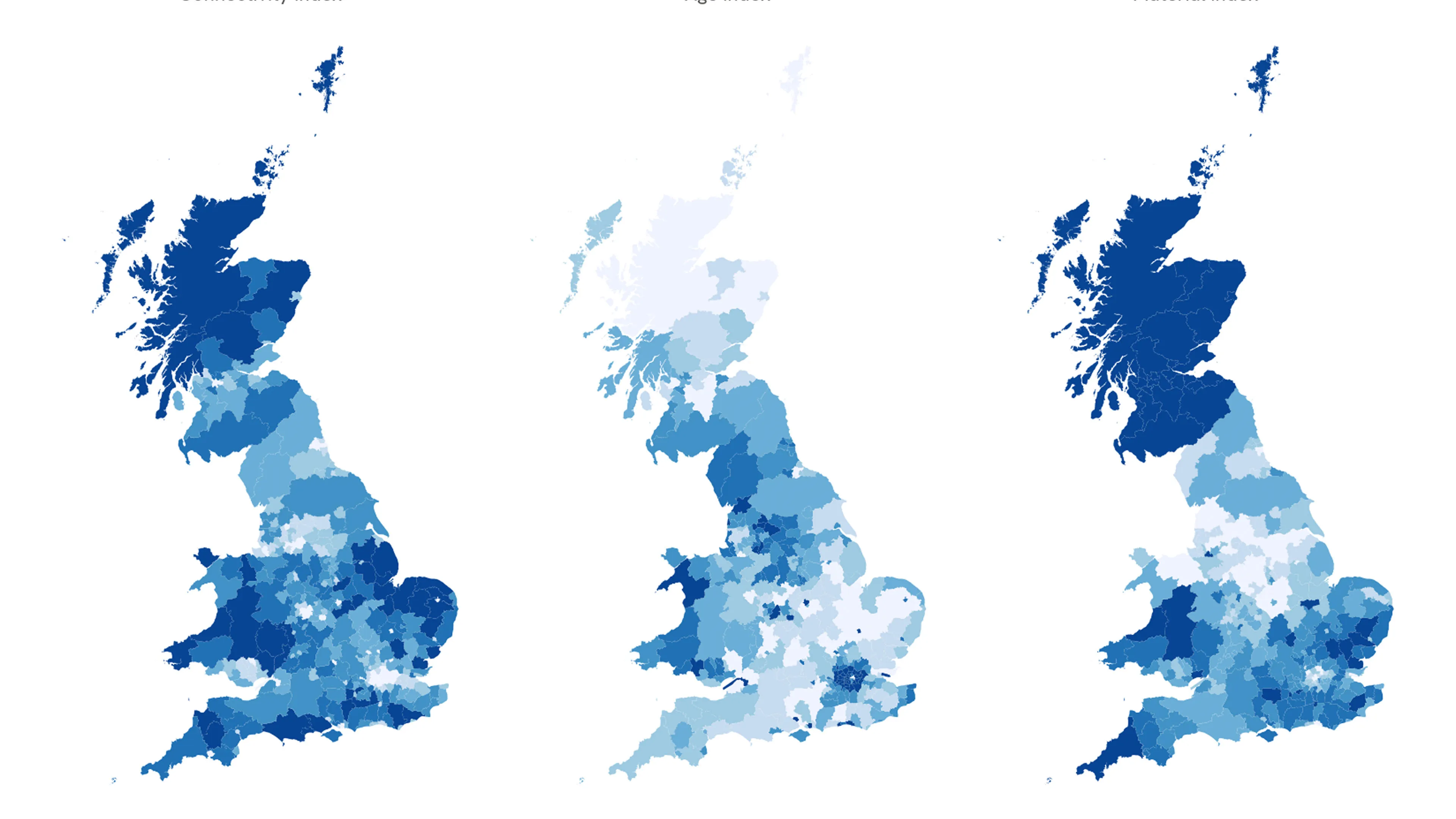

Improve customer satisfaction in telecoms with location data

Discover how accurate location data can unlock tailored services that align with regulatory requirements and customer needs.

Helping telecoms reach the next level of automation

Discover how accurate location data enables telecoms operators to automate network planning, site selection, and infrastructure deployment.